Advanced Micro Devices (AMD) presents a compelling investment opportunity within the burgeoning AI landscape. Unlike its primary competitor, Nvidia, which predominantly focuses on AI model training, AMD has strategically positioned itself to capitalize on the expanding AI inference market. This distinction is crucial, as inference, the process of utilizing trained AI models to make predictions and decisions, is projected to be a larger and more sustainable market than training. AMD’s diversified approach, encompassing CPUs, GPUs, and specialized accelerators, allows it to effectively address the varied computational needs of inference workloads, offering cost-efficient solutions compared to Nvidia’s high-end GPU-centric approach. This strategic divergence positions AMD for robust growth, potentially outpacing Nvidia in the medium term.

AMD’s financial performance further strengthens its investment appeal. The company’s data center segment, a key driver of growth, has exhibited substantial year-over-year expansion, signaling its increasing prominence within the AI infrastructure market. While Nvidia currently commands a dominant share of the AI GPU market, AMD’s focus on inference and its open-source software ecosystem, ROCm, provide it with a competitive edge. ROCm enables broader compatibility and reduces reliance on Nvidia’s proprietary CUDA platform, further enhancing AMD’s appeal to cost-conscious customers. Projections for the next two to three years suggest a compound annual growth rate of over 35% for AMD’s earnings without non-recurring items, fueled by the ongoing AI boom and diversified revenue streams. This growth trajectory is further supported by anticipated revenue growth of around 20% annually over the same period.

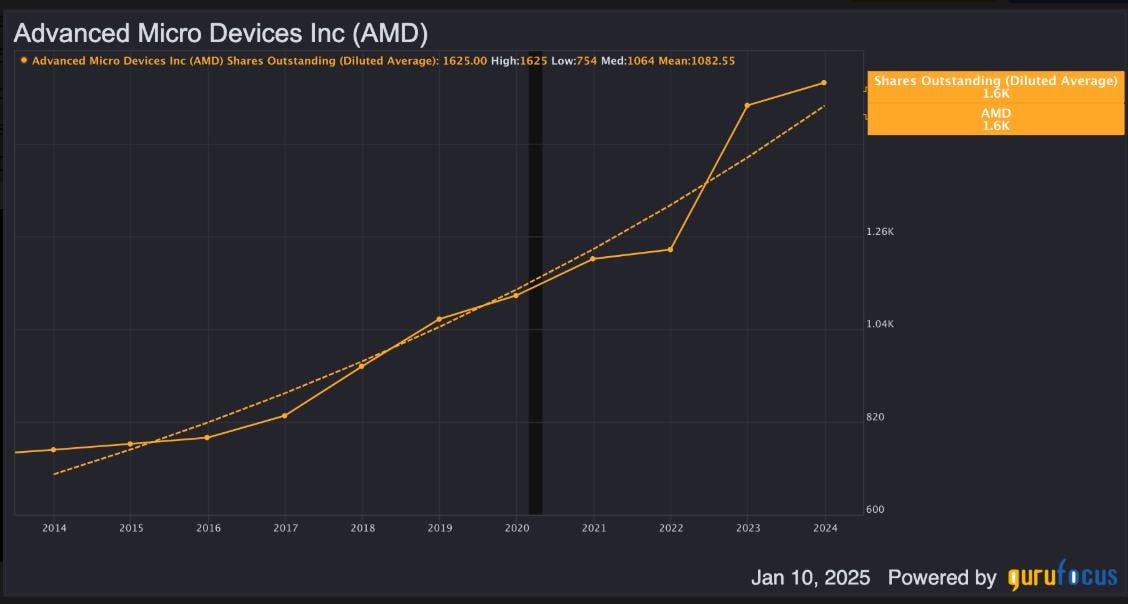

A detailed valuation model reinforces the bullish outlook for AMD. Considering a projected slowdown in share count growth due to increased profitability and reduced reliance on equity financing, the model forecasts earnings per share without non-recurring items of $8.37 for Fiscal 2027. This projection is based on an estimated annual revenue of $44.5 billion and a net margin of 35%. Compared to its historical valuations and industry benchmarks, AMD’s current price-to-earnings and price-to-sales ratios suggest an attractive entry point for investors. Applying a conservative terminal multiple of 35, consistent with historical data and industry norms, the model yields a December 2027 price target of $290, implying a compound annual growth rate of over 35% for the next three years.

The current discounted intrinsic value of AMD stock, calculated using a weighted average cost of capital of 16.83%, stands at $180. With the stock currently trading around $115, this represents a significant margin of safety of approximately 35%. This margin provides a buffer against potential market fluctuations and underscores the compelling risk-reward profile of investing in AMD. The company’s strategic focus on the high-growth AI sector, coupled with its diversified product portfolio and cost-effective solutions, positions it for sustained success in the long term.

Despite the positive outlook, it is important to acknowledge potential risks associated with investing in AMD. While the company’s concentration on AI presents significant growth opportunities, it also exposes it to industry-specific challenges. Fluctuations in AI spending patterns, potential technical issues with its products, and competition from established and emerging players in the AI accelerator market could impact AMD’s performance. Companies like Broadcom and Marvell, as well as niche players like Cerebras and Groq, are vying for market share in the AI landscape, posing a competitive threat to AMD’s ambitions.

Furthermore, geopolitical factors, such as ongoing tensions between the East and West and potential disruptions to global supply chains, represent external risks that could affect AMD’s operations. Navigating these challenges will require strategic agility and continued innovation. However, AMD’s current trajectory, marked by strong financial performance, a clear strategic vision, and a compelling valuation, suggests that it is well-positioned to capture the long-term demand for AI computing and deliver substantial returns for investors. The company’s focus on inference, coupled with its diversified product strategy and commitment to open-source solutions, sets it apart in the competitive landscape and provides a strong foundation for future growth.