")

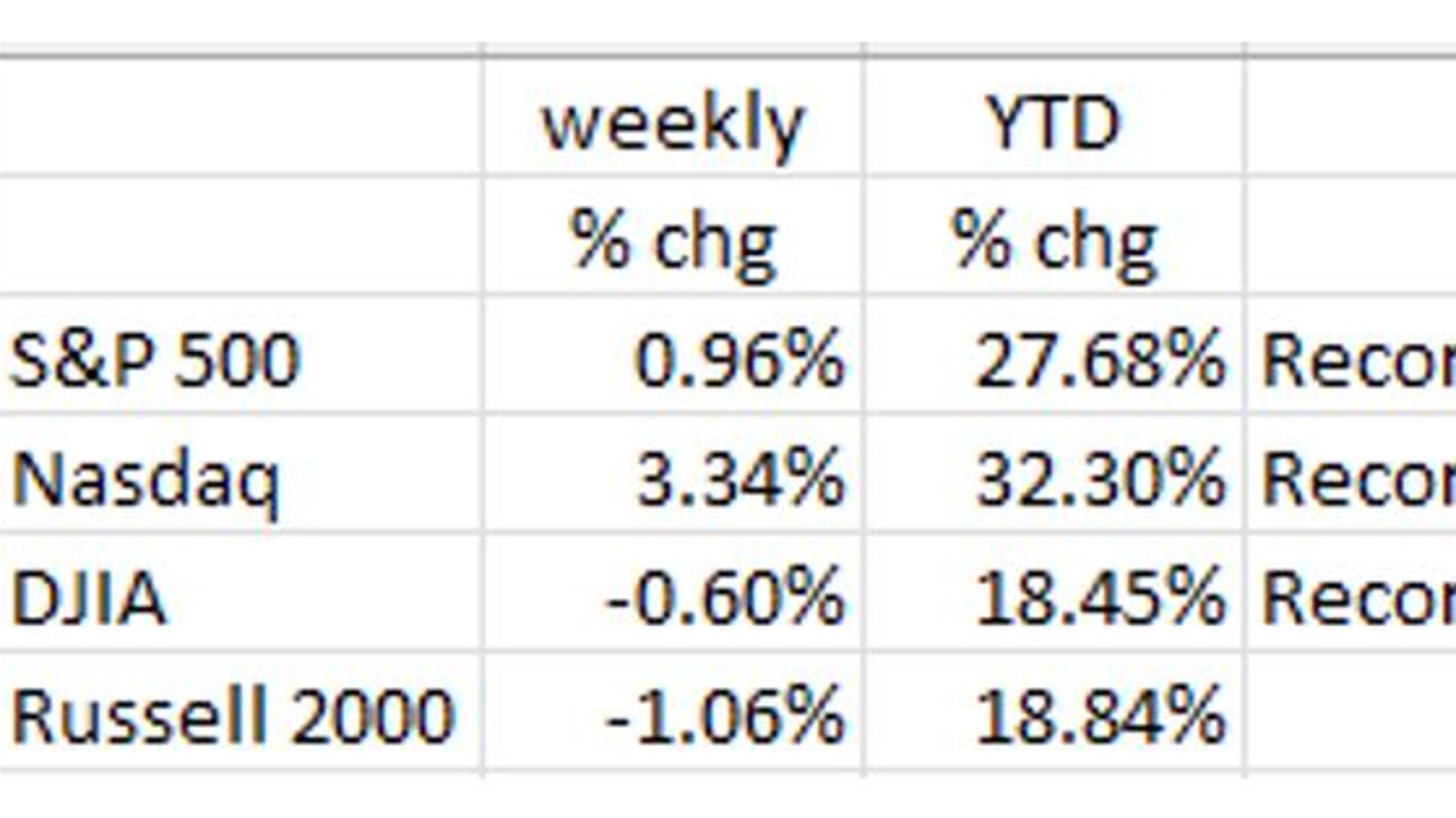

The financial markets experienced a week of anticipation culminating in the release of November’s jobs data, which proved to be a “Goldilocks” scenario – neither too hot nor too cold. This positive sentiment propelled the S&P 500 and Nasdaq to record closing highs on Friday, December 6th, with the S&P 500 gaining nearly 1% for the week and the Nasdaq soaring by an impressive 3.3%. The Dow Jones Industrial Average, while slightly down for the week, also achieved a record high mid-week. The outlier was the Russell 2000, representing small-cap stocks, which declined by just over 1%. The Nasdaq’s exceptional performance was fueled by strong gains in the “Magnificent Seven” tech giants, with several hitting new highs during the week.

The employment landscape presented a mixed picture. ADP’s private payroll report indicated slower job growth in November compared to October, with notable weakness in small businesses. The official Non-Farm Payrolls report, however, showed a gain of 227,000 jobs, aligning closely with market expectations and suggesting continued economic expansion. However, a deeper dive into the data reveals underlying concerns. The Birth/Death model, used to estimate small business activity, added 101,000 jobs to the headline number, a figure potentially inflated due to the rise in small business bankruptcies. This adjustment brings the actual counted jobs down to 126,000. Furthermore, the Household Survey, a more reliable indicator of economic turning points, painted a contrasting picture with significant job losses for the second consecutive month, reaching levels not seen since the onset of the COVID-19 pandemic. This survey also revealed substantial job losses among prime-age workers, raising concerns about the overall health of the labor market.

A sectoral breakdown of job changes reveals that gains were concentrated in Government, Healthcare and Social Assistance, and Leisure/Hospitality, while the Retail sector experienced a notable decline, shedding 28,000 jobs. This aligns with reports of retailers’ cautious outlook for the holiday shopping season and the slowest expected sales growth in six years. Increased initial unemployment claims in several states further corroborated the weakening labor market narrative. Data from the Job Openings and Labor Turnover Survey (JOLTS) also points to a cooling labor market, with job openings declining significantly from their peak in March 2022 and returning to pre-pandemic levels. The gap between hirings and job openings suggests a continued softening in labor demand. Layoff announcements tracked by Challenger, Gray & Christmas further underscore this trend, reaching levels comparable to the recessionary period of 2020.

Consumer sentiment appears to be weakening, with major retailers reporting increased price sensitivity and resistance to price hikes among consumers. This shift in consumer behavior is reflected in the extended Black Friday sales period, which began a month earlier than usual, likely an attempt to stimulate demand in a challenging economic environment. Rising delinquency rates for credit card and auto loans suggest that consumers, particularly those at the margin, may be facing financial strain. This combination of factors – cautious consumer spending, declining retail employment, and extended promotional periods – suggests a potential slowdown in economic growth.

Despite a robust GDP growth rate of nearly 3% for much of 2024, the aforementioned indicators, including weakening consumer sentiment, declining retail activity, and rising delinquencies, point towards a potential economic deceleration. The latest Quarterly Census of Employment and Wages (QCEW) indicates wage growth of 4%, coupled with a 2% productivity growth rate, resulting in a net inflationary pressure of 2%, aligning with the Federal Reserve’s target. Excluding the lagged rent data used in CPI calculations, inflation appears to be even lower, potentially below the Fed’s target. With real-time rent data continuing to show negative growth, the expectation is for lower CPI figures in 2025.

Despite hawkish rhetoric from some Federal Reserve officials, the weakening consumer and slowing labor market are expected to influence monetary policy. It is anticipated that the Fed will lower the federal funds rate by 25 basis points at its December meeting, moving towards a neutral rate of 3%. This easing of monetary policy is viewed as positive for the bond market. Equity markets, however, continue to exhibit frothy valuations, with all major indices reaching record highs despite the underlying economic concerns. The divergence between the buoyant equity market and the weakening economic indicators raises questions about the sustainability of the current market rally. The combination of a cooling labor market, softening consumer spending, and easing inflation creates a complex economic picture, suggesting a potential shift in the economic landscape as we move into 2025. While the equity markets remain optimistic, the underlying data warrants a cautious approach, as the confluence of these factors could impact future economic growth and market performance.